This post looks at the reasons behind recent bond performance as well as explores what role bonds may serve in our client’s portfolios moving forward.

Written by Karen Folk, CFP®, Ph.D., Founder & Advisor Emeritus of Bluestem Financial Advisors

Both my husband and I have been loyal clients of TIAA (formerly TIAA-CREF) for over thirty years. Throughout our academic careers, we chose TIAA over several possible providers. We were attracted to their low cost mutual funds and long nonprofit heritage of service to teachers. Founded in 1918 as the Teachers Insurance & Annuity Company to help teachers retire comfortably, they have become a leading retirement plan provider for academic, research, medical, cultural and government employees.

Recently, as an account holder, I have grown concerned by TIAA’s behavior towards us as consumers. We have noticed increasing encouragement by TIAA representatives to consolidate and rollover other retirement assets to their platform. We were notified in 2015 that TIAA had appointed a full-time representative locally. We were subsequently contacted on multiple occasions asking us to meet with this representative. After researching this individual on LinkedIn, I noted his past experience included sales roles with other large brokerage firms, but listed no Financial Planning credentials beyond the minimum required licenses.

A recent New York Times article “The Finger-Pointing at the Finance Firm TIAA” (October 21, 2017, Gretchen Morgenson), revealed some rather dramatic changes in TIAA that have led to whistleblower complaints to regulatory agencies as well as a lawsuit. The whistle-blower complaint filed with the Securities and Exchange Commission, obtained by The Times, “was filed by former TIAA employees who contend they were pressured to sell products that generated more revenue for the firm but were more costly to clients while adding little value”. This was followed by the NY Times article “TIAA Receives New York Subpoena on Sales Practices” (Nov 9, 2017). The NY state attorney general has subpoenaed records from TIAA to investigate possible regulatory infractions.

Both articles increased my concerns about whether the changes I noticed at TIAA are contrary to their long tradition of unbiased advice at low cost. As we investigated further, my husband was surprised to learn that parts of TIAA stopped being a nonprofit in 1997 – he, and I am sure many other TIAA clients, was not aware that much of TIAA is now a for-profit enterprise.

The NY Times October 21st article explains that, in 2005, TIAA established the Wealth Management Group. This group offers investment management services for a fee, a fee which is in addition to the underlying administrative and investment fees charged by TIAA funds. The lawsuit and whistleblower complaints claim that TIAA’s Wealth Management Group, now called “Individual Advisory Services”, is pushing customers into higher-cost products that generate higher fees. Given that TIAA continues to highlight its nonprofit heritage and its salaried employees, my concern is that TIAA clients are not aware of this conflict of interest.

Based on my own experience, experiences reported to us by clients, and the NY Times articles, we did some additional research we thought worth sharing.

We started by reading TIAA’s Form ADV, Part 2A, of the TIAA Advice & Planning Services’ (“APS”) Portfolio Advisor Wrap Fee Disclosure Brochure. The ADV is a public disclosure document required by the Securities and Exchange Commission (SEC) of all professional investment advisors. The Form ADV discusses investment strategy, fee arrangements and service offerings. In my opinion, the relevant items are:

Compensation arrangements. In the “Advisor Compensation” portion of the ADV, TIAA states several times that “The compensation does not differ based on the underlying investments chosen within the solution, nor does the Advisor receive any client commissions or product fees.” While true, these “salaried” advisors do in fact earn “credits” towards their annual variable bonuses based on a number of factors. The ADV states clearly, “the annual variable bonus gives Advisors a financial incentive to enroll and retain client assets in the program” (i.e. a managed fee account, more complex solutions, or other TIAA products such as life insurance). The ADV states again that “Advisors have an incentive to and are compensated for enrolling and retaining client assets in TIAA accounts, products and services, but do not receive any client commissions or product fees.” Advisors are also compensated for “gathering, retaining, and consolidating” any new TIAA client accounts that they persuade clients to transfer to TIAA from other brokers (e.g. Morgan Stanley, Fidelity, Merrill Lynch, etc.).

In addition to the base salary received by all advisors, TIAA provides additional compensation in the form of variable annual bonuses to individual advisors. These bonuses are determined not only as a percentage of the amount of assets under management advisors accumulate, but also by the amount of wealth advisors are able to transfer from existing funds into their TIAA managed brokerage accounts. This means, that, while advisors receive a base salary (“no client commissions or product fees”), the bonus structure heavily influences advisors to move client assets to new managed accounts with added management fees, and to sell complex solutions (i.e., TIAA annuities or TIAA insurance) to their clients. In my opinion, this adds a conflict of interest similar to that of conventional brokers who receive higher commissions for selling certain products or certain funds. Yet, TIAA continues to emphasize its “no client commissions or product fees” mantra.

My additional concern about TIAA is that their recent more aggressive sales tactics seek to funnel existing TIAA clients nearing retirement into much higher cost TIAA Advice & Planning Services Advisor managed accounts. Enrolling in these accounts could result in retirees unknowingly paying additional fees to the advisor on top of the mutual fund fees they now pay in their current TIAA accounts. Accepting a TIAA Advisor’s Advice & Planning Services proposal contract includes substantial additional fees which may not be apparent to a customer who does not mine the depths of the lengthy ADV, Part 2 disclosure document.

How much would an unsuspecting TIAA client who converted to a TIAA Advisor wrap fee account pay annually? The TIAA fee schedule for Advisor & Planning services accounts is an asset-based program fee. (reproduced below from the Form ADV):

If a TIAA client with $500,000 in assets chose to work with a TIAA Advice & Planning Services advisor in a program account, their annual fees (in addition to annual mutual fund fees) would be $4,925; for a client with $1,000,000 in investments accounts, their annual fees would be $8,925. My concern is that TIAA clients contacted by or directed to a local TIAA advisor may not understand or realize the higher fees that come with that advisor’s proposals.

A final concern deals with TIAA directing existing clients to their local representative for a “review”, as we personally experienced. That “review” comes with a hidden incentive for the local representative to propose an advisor managed account. In addition to our being contacted by phone several times, the TIAA website has been redesigned to feature a prominent “My Advisor” icon on every page in the upper right. Existing clients who login to view their accounts and use that icon are directed to call their local TIAA representative. Why is the local representative “My Advisor” rather than TIAA representatives reachable by phone whom we have dealt with in the past?

TIAA has an exemplary not-for-profit heritage of serving education professionals with low cost, well-rated funds. While the TIAA Board of Overseers continues their service to nonprofit employers, the new TIAA Advice & Planning services business structure follows a more common brokerage firm model. Specifically, the way their advisors are compensated appears to incentivize TIAA salaried employees to steer clients to higher cost managed accounts and other insurance products and to gather additional assets held outside TIAA. I believe that this managed account model introduces a conflict of interest for advisors to serve the best interests of TIAA clients. Per the TIAA whistleblower’s complaint, this bonus compensation structure pushes advisors to move clients into products “more costly to clients while adding little value”. While a TIAA advisor’s proposed investment portfolio may appear more diversified due to including a larger number of TIAA funds, the client’s original choices of fewer funds without the managed account fee may serve that client’s interests just as well at a much lower cost.

In addition, a TIAA advisor managed account provides solely investment advice. While tailored to your “goals”, I believe investment decisions should be made in the context of a comprehensive financial plan, not as an isolated component. Without incorporating tax planning, management of other risks and a detailed cashflow analysis, tailoring an investment portfolio to “your goals” can lead to unintended consequences, especially when making decisions about retirement income from a portfolio. As for financial planning advice, I recommend consulting a trained Certified Financial Planner™ professional who, as a fiduciary, is bound to act in your best interests. Why pay TIAA to manage your accounts when, for a similar fee, a fee-only planner can provide a financial plan that includes portfolio management in the context of a comprehensive plan?

While Bluestem Financial Advisors continues to enjoy a strong working relationship with TIAA through the SURS state retirement program, transparency is of the utmost importance to us, and we hope it is for you as well. Buyer beware: a proposed portfolio promoted to you by your local TIAA advisor may come with much higher ongoing expenses than just continuing to self-manage your original lower-cost TIAA mutual fund choices.

The U.S. Department of Labor just released its long-awaited fiduciary rule. The new rule aims to protect consumers saving in retirement accounts by amending the definition of fiduciary. The rule, in the pipeline for several years, applies to IRA, 401k, 403b and other retirement accounts that fall under the Employee Retirement Income Security Act (ERISA). Advisers and Brokers giving advice on investments in retirement accounts will now be required to act in the client’s best interest, i.e. when they offer advice on investment products in retirement accounts they must provide impartial advice and avoid conflicts of interest. Prior to this, they were only required to sell “suitable” investments to clients. While the rule does make a gallant effort to protect consumers, it also gives many concessions to commission sales-focused advisers. The rule implementation timeline was extended to January 1, 2018 (causing many to argue this simply gives more time for large companies to fight the rule); the rule also allows brokers to continue to sell certain products as long as they enter into a legal contract with the consumer that, among other things, discloses any conflicts of interest. How many consumers will read and understand such contracts? The rule has received considerable opposition from large investment firms, mainly those in the industry who are heavily sales-focused. Their major complaints revolve around new compliance regulations and the fact that the rule will dramatically alter their former commission based-sales approach. The prior “suitability” rule has no requirement to put the consumer’s best interest above the advisor’s interests.

While many in the financial services industry are upset by the new rule, others, like Bluestem, welcome the new consumer protections and are thrilled that the DOL is making an effort to help protect individuals saving for retirement. As a Fiduciary, Registered Investment Advisor, Bluestem always has and always will put our client’s best interest first. We are proud to be a fee-only financial planning firm and will continue to offer unbiased advice and stellar service to all of our clients. While other firms need regulatory nudging to get on board with fiduciary standards, we live by them every day. In fact, the financial planning organizations we belong to, NAPFA and ACP, believe that the new rule is a step in the right direction to add much needed consumer protections.

So how does this DOL rule affect Bluestem? In a nutshell, it doesn’t. It’s very possible that there may be some new regulatory compliance procedures for us, but in the big picture, Bluestem isn’t making any changes. Bluestem is passionate about fee-only, no product sales, financial planning. It’s this passion for fee-only planning that has kept us on the right side of this issue from the beginning. While others will be clamoring to further water down the new rule or put up a fight to protect their outdated and biased way of offering “financial advice”, Bluestem will continue our efforts to provide trusted, clear-cut advice and spread the word about our professional fee-only alternative to product sales masquerading as financial planning.

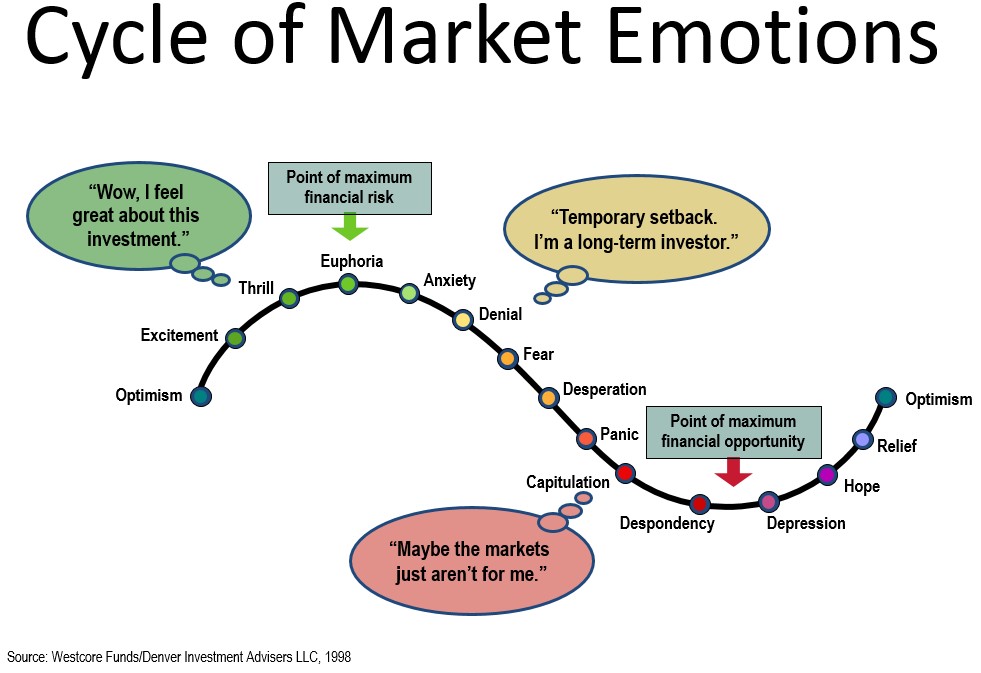

You are probably aware of the stock market activity over the past week. Friday saw the largest drop of the week, rounding out weekly losses in the 5-6% range. This, in turn, fueled massive negative media coverage over the weekend. No doubt, the negative news adds to fears and is one of many factors leading to further losses in the market. As usual, we encourage you to hold steady through the current market gyrations. One soundbite repeated over the weekend news cycle is that the market has not seen a single day drop like Friday’s since 2011. Do you remember which day it was? My guess is that, unless the last drop significantly affected your life or financial plans, the answer is no. The uncertainty of the future can be scary. Our natural first reaction is fear and trying to avoid further losses. Our brains are hardwired to react this way. However, acting on this emotion would be a mistake. It would lead to selling when the market is low, when in reality, that is the complete opposite of the approach you should be taking. The chart below illustrates this.

I predict one of two possible outcomes of the market in the next year:

1. The market will continue to decline as the world economy sorts through its current concerns. For our retiree clients, they will ride the downturn relying on the safety of their bond ladders without fear of where their next paycheck is coming from. For our working clients, they will keep working, contributing regularly into the market and buying stocks while they are on fire sale. Over the long term, the market will recover!

2. The market will recover in the next few weeks and we will quickly forget about the conditions of the past week.

Cycles such as the one we are currently experiencing are part of investing. Doing nothing when the market is getting a little haywire may seem counterintuitive or that we are avoiding the problem. The reality is that sticking to a long term plan through market changes takes resolve and commitment to the stated investment goals. Fighting instinct is hard, but doing so leads to better investment performance in the long run and, more importantly, a better chance of realizing your financial goals.

My home to office commute averages around 12 minutes, during which I enjoy listening to the news to catch up on current events. During my commute the day’s stock market figures are also announced. As a Financial Planner this information may seem useful, but it is not. Below are some of the reasons why I believe this information can be counterproductive.

It is no accident that Las Vegas casinos use chips and tokens instead of actual money when playing their games. It tricks our brains into separating the value of the chips from the cash value the chip represents. Stock indices and the underlying stock prices have somewhat of the same effect. Individuals cannot easily mentally calculate a stock market point change into a tangible effect on their wealth. To do so, they would need to:

All of this work only to realize these index quotes relate only to a single day.

Stock tickers only tell you the change in one particular market segment for a particular segment of time, usually that day. For most people, that information has little relation to daily life. Even Charles Dow, founder of the Dow Index, did not watch his own index on a daily basis.

When investing in the stock market, you must take an ownership mentality. A stock is a partial ownership in a company, entitling you to a share of future income. Any business owner may benchmark her business’ performance on a regular basis. That process is helpful to evaluate areas of success, weakness and future opportunities. However, this process would not be repeated daily, weekly or likely even monthly. It would be too time consuming, confusing and not likely to produce useful information.

Too much time spent on daily monitoring of the stock market takes time away from activities that could be more productive.

Far too much attention gets placed on the investment component of individual’s personal financial situations. It is an important component, to be sure. There are plenty of examples of individuals who struck it rich from the one right pick. For every case of one lucky decision, there are many more stock picks that only produced average or even below average performance that we don’t hear about. For most people, long term wealth is built through a series of small decisions. Spending too much time focusing on investments takes time away from making those good decisions.

Time spent on investing should be focused on selecting an appropriate level of risk for your goals and situation, building a diversified portfolio of low-cost funds, sticking to an investment philosophy and regular review and rebalancing. Once this foundation is established, annual or biannual investment reviews leave time to focus on other value-added activities such as proactive tax planning, setting and updating goals, and managing behaviors to meet those goals.

For these reasons, you will never see a stock market ticker quote on our website. I do not look at these figures on a daily basis and for your financial health, I suggest you refrain from checking them daily as well.

If you read the rest of this post, you will find my title to be a bit flippant. Had I added the work "Quickly" to the end, it would be downright misleading. Except for the rare instance where someone inherits a fortune, wins the lottery or marries a multi-millionaire, getting rich is a slow and boring process. This fact is mostly overlooked by the media. Boring does not sell newspapers or generate web hits and therefore good financial advice is rarely a media event. That is why I was excited to see some press on a newly released e-Book written by Financial Advisor and author William Bernstein for Millennials (aka Gen Y, born 1980's through early 2000's). Concisely written, the book summarizes how to actually build financial freedom, aka wealth. Spoiler alert, the method is simple but the application will take effort on your part.

The book is so short, it is hardly worth summarizing on this post. You should seriously consider taking 30 minutes to read the ~14 page guide yourself. Purchase the e-Book for $0.99 on Amazon's Kindle Library or download free in PDF format.

What really resonates about this book is the simplistic method he advocates; live below your means (save 15%), educate yourself on the basics, keep the portfolio simple because you will not beat the market. These are all key parts of our approach to financial planning. Success comes not from taking big risks or complex strategies, but by being diligent and making good decisions.

I will not underplay the "making good decisions" factor. We are all human and we all make errors in judgment. Some errors are unavoidable, but others come from fear, greed or other emotional roadblocks. Decisions need to be made objectively in context of your current situation and future goals. Doing this on your own is incredibly difficult. Even the most savvy among us regularly make less than objective decisions. For many, this is the value of having a Financial Planner. To act as the objective, informed third party and provide a fresh perspective.

Be sure to check out some of the press on this book, including an interview on NPR's Here and Now and a summary by columnist Scott Burns.

This past week, the Federal Reserve Board announced they were not cutting back on their efforts to stimulate the economy. This surprised many investors, who had been expecting the Fed to begin tapering their bond buying program. The question many have is, how does this affect my own financial decisions? I had a chance to answer some of these questions on the September 20th Edition on Focus 580 with host Jim Meadows and guest Kevin Waspi.

How Should I React to this News?

Both Kevin and I agreed on the answer to this question: for most people this is just market noise that can be ignored. It is important to recognize the difference between an Investor, who is seeking gains by investing long term in companies and participating in the growth and income of those investments, and a Speculator, who attempts to profit by making bets on short term market movements. For most individuals, it is more important to focus on meeting long term goals through sticking to their investment plan. Speculating requires a lot more risk, knowledge and time than the average investor possesses.

What Does this News Mean about the Economy and my Portfolio?

One interpretation could be that the Fed is not optimistic about the recovery of the economy, which could be worrisome to investors. However, the Fed's decision is based on many factors including unemployment and inflation. They are in a delicate balancing act among many different factors.

Kevin pointed out that as the Fed does taper off their stimulus in the coming months or years, savers may benefit. It could be expected that interest rates would rise over the long term, resulting in higher yields on checking, savings and even bonds. In the short term, we should expect some volatility as investors try to gauge how market changes will affect future profits.

Check out the complete episode here. We also addressed many other questions including: