Recently, our own Jake Kuebler spoke with Investor's Business Daily's (IBD) Aparna Narayanan about ways young Advisors are adapting traditional business models by using new technology and social media. Jake’s experience as a young business owner, as well as his leadership on NAPFA Genesis, has given him ample insights into the changing landscape of financial planning. The article hits on several of these new ideas, which you can click here to read.

Kuebler Appears on WCIA's Current to Discuss Couples and Finances

This week, Bluestem’s own Jake Kuebler appeared on the WCIA 3 News program Current, where he sat down with Cynthia Bruno to discuss ways couples can successfully manage their finances. Jake provided tips to help couples be more transparent when it comes to money and their long term financial goals. Jake shared advice on several financial issues including: buying a first home, preparing for children, saving for college and cohabitating vs. marriage. Jake’s biggest advice for couples is to be intentional with their finances. He suggests that planning ahead and making solid decisions early on reduces the need for rushed decisions or limited opportunities in the future. Jake also shared his thoughts on savings, saying that couples should automatically save first and use what is left over for “fun money”. This approach helps couples achieve their goals and worry less about budgeting. We all know that financial issues can be a source of stress for couples, hopefully Jake’s optimism and helpful tips can be a positive influence on your own relationship.

You can watch the full segment below or visit the Current webpage at illinoishomepage.net.

Real Change Happens at the Margin

I recently finished my second half marathon, finishing the race just under my target time of two hours. While pleased with reaching a personal goal, there is nothing really compelling about my story. No overnight success, no major rise to overcome great obstacles. There was a time when running for fun would sound crazy, let alone running for hours on end. I started running 14 years ago to get into shape. I cannot say I really even enjoyed it at the beginning. My first runs were on a basement treadmill, 1 mile at a time. Soon a single mile was easy, so I pushed it to two and then three. For a challenge I decided to run a 5k, which lead to another and then another. Each time I aimed to cut my time by pushing my regular runs just a little faster and a little further. Each time I hit a goal, I moved the target just a little bit further. A little longer distance, a little shorter time.

My evolution has been slow and incremental. My progress from year to year is minimal, barely even noticeable. Review these changes over years, and the results are slightly more impressive. Change happened from minor adjustments made over time and the result of those adjustments compounded over time.

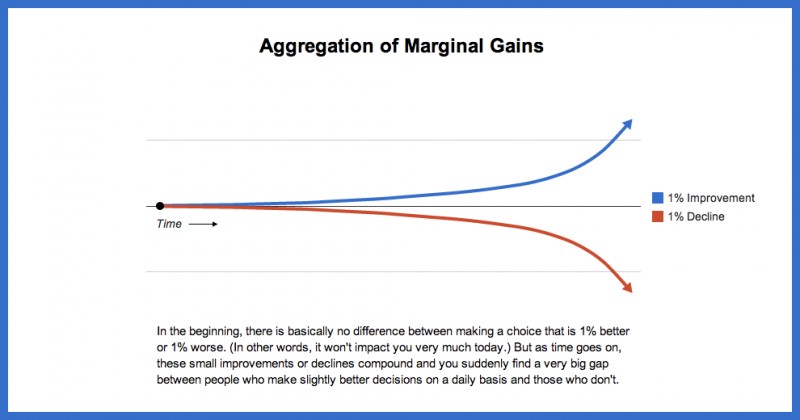

In a post appearing on The Daily Good, author James Clear outlines this same strategy. He describes how marginal changes led Great Britain’s cycling team to win the Tour de France in 2012 and 2013. Then, he shows the following illustration of how small changes, stacked onto one another lead to substantial changes over time.

This is a principle that we use daily with our Financial Planning clients. Big changes may happen at the beginning of our relationship, but planning is a long term process. An incremental series of good decisions and judgment based on an end goal will lead to long term success. As we work together year after year, we provide the long term perspective that keeps decision making on track and also reduces errors in behavior.

How can you apply this to your own financial life? Comment below if you want to share your own story.

Millennials' Guide to Getting Rich

If you read the rest of this post, you will find my title to be a bit flippant. Had I added the work "Quickly" to the end, it would be downright misleading. Except for the rare instance where someone inherits a fortune, wins the lottery or marries a multi-millionaire, getting rich is a slow and boring process. This fact is mostly overlooked by the media. Boring does not sell newspapers or generate web hits and therefore good financial advice is rarely a media event. That is why I was excited to see some press on a newly released e-Book written by Financial Advisor and author William Bernstein for Millennials (aka Gen Y, born 1980's through early 2000's). Concisely written, the book summarizes how to actually build financial freedom, aka wealth. Spoiler alert, the method is simple but the application will take effort on your part.

The book is so short, it is hardly worth summarizing on this post. You should seriously consider taking 30 minutes to read the ~14 page guide yourself. Purchase the e-Book for $0.99 on Amazon's Kindle Library or download free in PDF format.

What really resonates about this book is the simplistic method he advocates; live below your means (save 15%), educate yourself on the basics, keep the portfolio simple because you will not beat the market. These are all key parts of our approach to financial planning. Success comes not from taking big risks or complex strategies, but by being diligent and making good decisions.

I will not underplay the "making good decisions" factor. We are all human and we all make errors in judgment. Some errors are unavoidable, but others come from fear, greed or other emotional roadblocks. Decisions need to be made objectively in context of your current situation and future goals. Doing this on your own is incredibly difficult. Even the most savvy among us regularly make less than objective decisions. For many, this is the value of having a Financial Planner. To act as the objective, informed third party and provide a fresh perspective.

Be sure to check out some of the press on this book, including an interview on NPR's Here and Now and a summary by columnist Scott Burns.

Kuebler Appears on NewsChannel 15

This past week, NPR's Planet Money released an online tool comparing median income of various cities in relation to how far that income would go. Based on surveys by the Bureau of Economic Analysis, this tool draws on Regional Price Parity; measuring the variation in cost a basket of consumer goods would have in different locations. Especially of interest, the tool indicated residents of nearby Danville, IL see the biggest jump in "perceived" income due to the low cost of living in that area. ABC NewsChannel 15's Kim Shine sat down with our own Jacob Kuebler to discuss. You can see the full news story below.

You may also wish to see the full NPR story by following this link or the original NewsChannel 15 Story by following this link.

Planning for Rising University Tuition

This past week, the University of Illinois Trustees approved a tuition increase. News outlets immediately began reporting that the 4 year expected cost of attending the university now tops $100,000. How can parents plan for this? I was recently interviewed by Adam Rife of WICD News Channel 15 regarding how parents can plan for these changes. I offer a few points to keep in mind regarding this change. This recent announcement of $100,000 expected cost is as much a psychological barrier as an actual one. Similar to your car rolling from 99,999 miles to 100,000, the perception changes much more than the actual mechanics. However, rising costs are a troubling trend for parents planning for college education. For many years, college costs have been rising at about double the rate of increases in the cost of living.

In order to plan for the rising cost of higher education, my best advice as I told Adam is:

I think the key is always starting early, and unfortunately, starting early for most parents means you have a young child and there are a lot of other expenses coming up.

There are two important factors in saving for the future: Time and Dollars Saved. The more you have of one factor, the less you need of the other. Start early and you can save less and end up with more.

You should also keep in mind that the "Sticker Price" of college may not actually reflect the actual cost of attending college. Matching your student's skills and interests with a university or college can help them qualify for higher amounts of financial aid, scholarships and grants. In some cases, a smaller college with higher tuition may offer a more generous aid package to a desirable student than a larger public institution. We have found that College Navigator is one excellent resource for researching schools.

You can check out the full story here:

WICD NewsChannel 15 :: News - Top Stories - 4 Years Of UI Tuition To Top $100,000 For 1st Time.

Moving Jobs, Moving Retirement Plans - New York Times

Changing jobs can be a stressful event. At the same time you are learning new job responsibilities and acclimating to a new company culture, you have to juggle financial decisions such as choosing new employee benefits. An often neglected detail of this process is what to do with your old retirement plans. We often work with clients in “cleaning up” these old accounts that multiply and are lost track of over a career. With all the complexities of rolling over old plans, studies are showing many younger professionals are just cashing these plans out. I recently discussed this with Ann Carrns of the New York Times. I explain why I see this happening. Here is an excerpt from that article:

[Jake] says when young adults are switching jobs, money is often tight — they may be moving, and need financing for rental deposits and other costs — and it is tempting to withdraw the cash. In addition, he said, it is often difficult for them to envision retirement, when they are just starting their careers.

Besides the tax consequences of this action, which can be high, cashing out small retirement plans cheats the individual out of their most important asset — time. The more time you have in investing, the less you need to “save” to end up with the same pot of money at the end. By cashing out now, you are cheating your future self. By putting off savings, you end up saving more and ending up with less value at retirement.

It is easy to see why someone in their 20′s or 30′s would be so willing to make this trade-off. Retirement is an abstract concept many years into the future. I try to counteract this thought by aiming for a different goal. Replace the concept of “Retirement” with “Financial Independence”. Financial independence is having the freedom from working to support your lifestyle. Instead, you have the financial flexibility to work, volunteer or even not work and follow your passions.

The entire article was printed in the October 5th Edition of the New York Times, which you can read online by clicking this link.