Executive Summary

Bonds have long played a central role in the investment strategies we utilize with clients. Built as the “safety net” of the portfolio, some clients have been caught off guard with the losses bonds have seen in the last couple years. Bluestem still sees bonds as an important component of meeting various long and short-term investment goals. This post looks at the reasons behind recent bond performance as well as explores what role bonds may serve in our client’s portfolios moving forward.

What is Going On? Interest Rates and Risks

We have long regarded bonds as a safer alternative to stocks, and for good reason. At their core, a bond is like an “I Owe You” between an investor and the issuing organization. When you purchase a bond, you are loaning money to that organization. In exchange, you receive regular interest payments and the promise of your money back in the future. Unlike a stock, your rate of return is fixed through a promise of a pre-determined interest rate. Financial distress of the borrower could put this agreement at risk, but as a bondholder, you are legally entitled to get paid back ahead of stockholders (who fall to the back of the line).

While bonds may be less risky than stock, no investment is truly ever risk free. One major risk of bonds is Interest Rate Risk; the risk that bond values may change due to changes in interest rate. This risk arises because bond prices and interest rates have an inverse relationship—when interest rates rise, bond prices tend to fall, and vice versa. This is best illustrated by an example.

Example 1

Imagine you purchase a bond that for $10,000 that matures in 10-year with 3% annual interest payments (also called the coupon rate). If you hold the bond for the entire duration of the bond, you will receive $300 annually in interest and $10,000 when the bond matures.

However, if you wish to get your money back before the end of the 10-year term, you must find another investor to purchase the bond from you. If interest rates are higher than when you purchased, new bonds will be issued with higher coupon rates, making the existing bond less attractive to investors. Consequently, you would need to discount your bond enough to incentivize an investor to purchase your bond with a lower interest rate. This means the face value of your bond is worthless.

Example 2

Using the same example from above, imagine you wish to sell your bond with 5 years left on the term. Interest rates on new bonds with 5-year terms are paying interest of 4% or $400 per year. Your bond only pays $300 per year in interest. To entice an investor to buy your bond with lower annual interest, you must discount the face value of the bond from $10,000 to around $9,555¹.

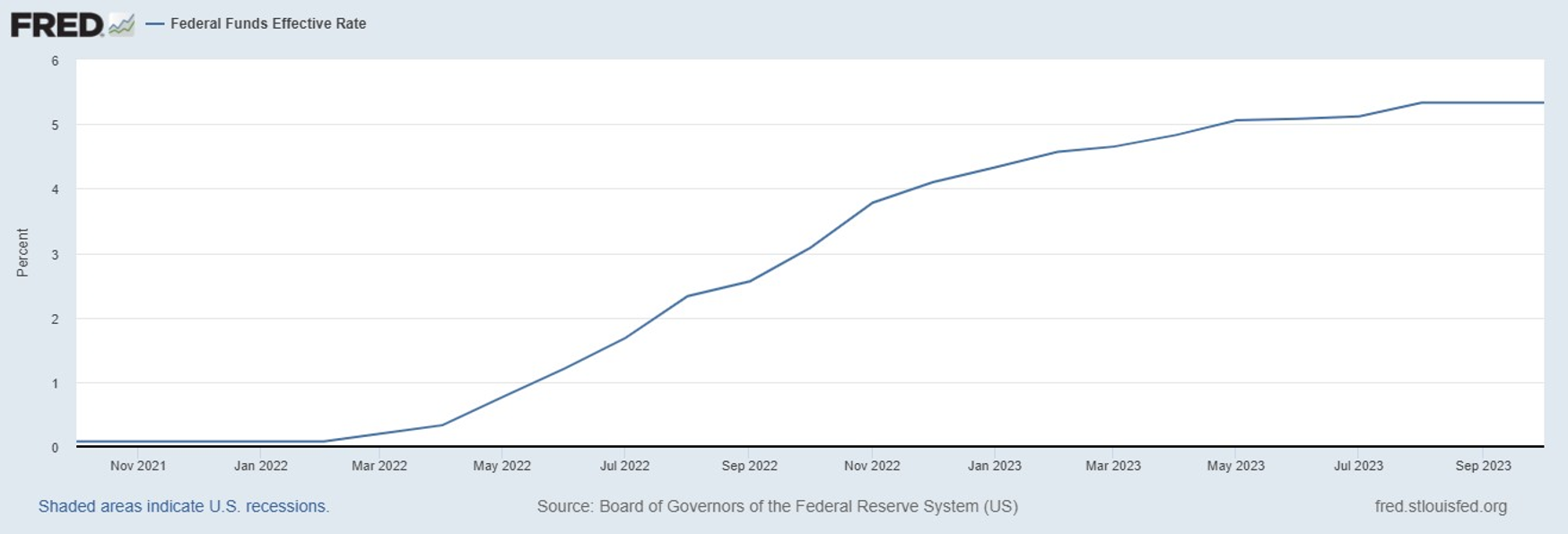

This is a major reason bonds have performed poorly over the past two years. In response to fears of inflation, the Federal Reserve Board has raised the Federal Funds Rate starting in early 2020. While this post will not explore the ties between monetary policy and market interest rates, these changes have pushed up investor expectations for interest rates. Bond values have fallen due to this inverse relationship. Here is an overview of how interest rates have increased over that period of time.

Fed Funds Effective Rate 10/01/2021 through 10/01/2023, Federal Funds Effective Rate (FEDFUNDS) | FRED | St. Louis Fed (stlouisfed.org)

Now compare that to the price of the Vanguard Total Bond Market Index (BND), which seeks to track the performance the Bloomberg U.S. Aggregate Float Adjusted Index. This Index measures the performance of a wide spectrum of public, investment-grade, taxable, fixed income securities in the United States. Using this as a proxy for bonds as a whole, you can see what happened to the bond fund’s value during the same time period.

Vanguard Total Bond Market Index Fund (BND), 10/01/2021 through 10/01/2023, BND Interactive Stock Chart | Vanguard Total Bond Market Index Fund Stock - Yahoo Finance

Re-Evaluating Bonds in Portfolio Allocations

With the rapid rise of interest rates over the past two years, the question comes up about what role (if any) should bonds play in portfolios going forward? To address this question, we really must think about what the goals of our clients and their portfolio are. Painting in broad strokes, we can generalize those goals in two client life stages:

⠀⠀⠀⠀⠀⠀⠀⠀Accumulator Mode - those who are building wealth for the future and do not ⠀⠀⠀⠀⠀⠀⠀⠀anticipate needing money from their portfolio for a longer period of time.

⠀⠀⠀⠀⠀⠀⠀⠀Conservation Mode – those who are financially independent and using their ⠀⠀⠀⠀⠀⠀⠀⠀portfolio to generate income to maintain their present lifestyle.

Bonds for Accumulators

Many argue that for young investors, a portfolio should be allocated to 100% stock. The argument is based on the long time-horizon of the investor, which allows the investor to take maximize risk for maximum reward. What this fails to account for is balancing the capacity for risk with the need and desire for risk. A colleague of ours, Bert Whitehead, often used this analogy:

⠀⠀⠀⠀Look at the risk in your portfolio this way. If you are flying from New York to Los Angeles, you could hire a fighter pilot who can demonstrate how fast the jet flies, how quickly he or she can maneuver, their skills are in steeply ascending and descending, and that their record flight is 4.25 hours. However, you also have the option to travel with a trained airline pilot who avoids bad weather systems, knows how to handle the jet streams, and is more concerned about the comfort and safety of your flight. Be aware that the airline pilot will estimate your time of arrival as 5.15 hours, but pads the schedule because the trip usually only takes 4.45 hours.

In other words, not everyone wants or needs to take maximum risk. Balancing returns with the comfort of the ride matters. Research consistently shows that the allocation between stocks and bonds is the most significant factor influencing overall portfolio returns². For clients in the accumulation phase, bonds play a crucial role in reducing portfolio volatility and providing a buffer against market downturns. Our philosophy emphasizes the importance of finding the right balance to achieve both growth and stability.

Bond for Retirees (Conservation)

For retirees, the need for a reliable source of income takes center stage. We have already established that the biggest risk of bonds is interest rate risk. However, this risk can be mitigated. If you hold the bond to maturity, the face value of the bond will be returned.

Example 3

Continuing the facts from Example 2, your bond was purchased with a face value of $10,000 but has dropped in value to $9,555 based on changes in interest rate. If you do not sell the bond now, the drop in value only reflects the market value other investors will pay you. The loss is “on paper” only. If you continue to hold the bond to its maturity, the face value will rebound until it matures at the original value of $10,000.

To ensure our clients do not need to sell bonds in environments of rising interest rates, we need to try and match up the bond maturity to when we anticipate clients will need income. We do this by setting up a series of bonds to mature annually that matches their expected spending. We call this the bond ladder. When pairing the bond ladder with a sufficient emergency fund, we can minimize the risk of needing to sell bonds during down markets

What is Next: The Silver Lining

If someone could reliably predict the future and impacts on interest rates, one could in theory use this information to tactically purchase and sell bonds to optimize movements in price. Without this information, the best we can do is make decisions on our individual goals and the information we do know to be true. This suggests that for our clients already holding bonds, we should continue to do so unless your goals or needs have changed.

There is some good news about continuing to hold bonds that have suffered losses due to interest rate increases. If you hold them to maturity, the value will recover as you approach maturity. This concept is illustrated above in Example 3 for individual bonds. Bond funds can be a bit more complicated to understand as they hold hundreds or even thousands of individual bonds packaged together as a single investment. Here is an example to help illustrate how a bond fund might perform.

Example 4

We earlier referenced the Vanguard Total Bond Market Index in the graph. At the time of this writing, the fund had an Average Duration of 6.1 years and Yield to Maturity of 5.6%³. The Average Duration approximates the average cashflow from coupon payments and bond maturities that would repay the current bonds price. Assuming no further changes in interest rates or losses from default, you would realize the Yield to Maturity if you can hold the bond without selling for that Duration Period.

Conclusion

In the face of a rising interest rate environment, our bond philosophy remains steadfast. We advocate for the strategic integration of bonds into our clients' portfolios, recognizing their role in providing stability, managing risk, and generating reliable income streams. As the financial landscape continues to evolve, rest assured that we are committed to adapting our strategies to ensure the financial well-being of our clients.

Footnotes

[1] Hypothetical value using the present value of an investment with a 4% discount rate, term of 5 years, and $300 annual interest payment, and $10,000 future value.

[2] Tactical vs strategic asset allocation (vanguard.com)

[3] Characteristics as of 10/31/2023, access from BND-Vanguard Total Bond Market ETF | Vanguard on 11/28/2023